Event held online

Conference proceedings

ECB Forum on Central Banking, November 2020

1

Contents

Programme 3

Central banks in a shifting world: takeaways from the ECB’s online

Sintra Forum 5

By Philipp Hartmann and Glenn Schepens

Monetary policy in a pandemic emergency 20

By Christine Lagarde

De-globalisation? Global value chains in the post-COVID-19 age 28

By Pol Antràs

De-globalisation? The recent slowdown of global trade and prospects

for future rebalancing 81

By Susan Lund

Macro-financial implications of climate change and the carbon transition 90

By Frederick van der Ploeg

Discussion of "Macro-financial implications of climate change and the

carbon transition" by Frederick van der Ploeg 143

By Signe Krogstrup

The decline in r* and the ECB strategy 151

By Jordi Galí

Informal central bank communication 156

By Annette Vissing-Jorgensen

The decline in euro area inflation and the choice of policy strategy 169

By Volker Wieland

Monetary policy challenges from falling natural interest rates 186

By Klaus Adam

Discussion of “Monetary policy challenges from falling natural interest

rates” by Klaus Adam 210

By Argia M. Sbordone

Fiscal rules, policy and macroeconomic stabilization in the euro area 221

By Evi Pappa

Discussion of Evi Pappa’s “Fiscal rules, policy and macroeconomic

stabilization in the euro area” 265

By Vitor Gaspar

De- and inflationary traps: strengthening ECB’s second pillar to avoid

fiscal and financial dominance 275

ECB Forum on Central Banking, November 2020

3

Programme

Wednesday, 11 November 2020

14:00-14:30 Introductory speech

Christine Lagarde, President, European Central Bank

Session 1: Implications of fundamental global changes for

central banks

14:30-15:30 De-globalisation? Global value chains in the post-COVID-19

age

Pol Antràs, Professor, Harvard University

Discussant: Susan Lund, Partner, McKinsey Global Institute

Chair: Luis de Guindos, Vice-President, European Central Bank

15:30-15:45 Break

15:45-16:45 Macro-financial implications of climate change and the carbon

transition

Frederick van der Ploeg, Professor, University of Oxford

Discussant: Signe Krogstrup, Governor, Danmarks Nationalbank

Chair: Luis de Guindos, Vice-President, European Central Bank

16:45-17:00 Break

17:00-18:00 Panel: Inflation objective, structural forces and central bank

communication

Jordi Galí, Professor, Universitat Pompeu Fabra

Annette Vissing-Jørgensen, Professor, University of California,

Berkeley

Volker Wieland, Professor, Goethe University Frankfurt

Chair: Philip R. Lane, Member of the Executive Board, European

Central Bank

ECB Forum on Central Banking, November 2020

4

Thursday, 12 November 2020

Session 2: Macroeconomic stabilisation frameworks in a new

economic environment

14:00-15:00 Monetary policy challenges from falling natural interest rates

Klaus Adam, Professor, University of Mannheim

Discussant: Argia Sbordone, Vice-President and Function Head,

Macroeconomic and Monetary Studies Function, Federal Reserve

Bank of New York

Chair: Fabio Panetta, member of the Executive Board, European

Central Bank

15:00-15:15 Break

15:15-16:15 Fiscal rules, policy and macroeconomic stabilization in the

euro area

Evi Pappa, Professor, Unversidad Carlos III Madrid

Discussant: Vítor Gaspar, Director, Fiscal Affairs Department,

International Monetary Fund

Chair: Yves Mersch, Member of the Executive Board, European

Central Bank

16:15-16:30 Break

16:30-17:30 Panel: Monetary policy instruments and financial stability

Markus Brunnermeier, Professor, Princeton University

Lucrezia Reichlin, Professor, London Business School

Hyun Song Shin, Economic Adviser and Head of Research, Bank

for International Settlements

Chair: Isabel Schnabel, member of the Executive Board, European

Central Bank

17:00-17:45 Break

17:45-18:45 Policy panel

Andrew Bailey, Governor, Bank of England

Christine Lagarde, President, European Central Bank

Jerome H. Powell, Chair of the Board of Governors of the Federal

Reserve System

Moderator: Roula Khalaf, Editor, Financial Times

18:45 Young economists’ award announcement and closing remarks

ECB Forum on Central Banking, November 2020

5

Central banks in a shifting world:

takeaways from the ECB’s online Sintra

Forum

By Philipp Hartmann and Glenn Schepens

1

Abstract

The 2020 ECB Forum on Central Banking was designed to analyse the implications

of selected key structural changes that have a bearing for how monetary policy

works in the euro area and to combine this with discussions on selected core topics

featuring in the European Central Bank's review of its monetary policy strategy. In

this article, two of the organisers highlight some of the main points from the papers

and discussions, including whether the globalisation of trade and supply chains

shows signs of a reversal, macro-financial implications of climate change and the

carbon transition, options for formulating the ECB's inflation aim with a low natural

rate of interest, challenges with informal monetary policy communication,

relationships between financial stability and monetary policy, how to make a

monetary policy framework robust to deflation or inflation traps and how fiscal policy

can contribute best to the economic recovery from the COVID-19 pandemic.

1 Introduction

Geopolitical developments, climate and demographic change, technological

innovations and, most recently, the COVID-19 pandemic have triggered fundamental

changes to the economies in which central banks around the world are operating. It

is in this context that the ECB is conducting the review of its monetary policy

strategy. The 2020 ECB Forum on Central Banking was one of the “ECB listens”

events through which the ECB collects the views of relevant outside parties on its

monetary policy framework. Policymakers, academics and market economists

debated the implications of selected key structural changes that have a bearing for

how monetary policy works in the euro area, combined with discussions on core

topics featuring in the strategy review. In this chapter we summarise some of the

main issues debated and group them in five themes: fundamental structural changes

in the world economy; formulations of central banks' inflation aim close to the

effective lower bound of nominal interest rates; formal versus informal monetary

policy communication; monetary policy, the allocation of risk and central bank

1

Philipp Hartmann is the Deputy Director General for Research and Glenn Schepens a Senior

Economist in the European Central Bank's Directorate General Research. Any views expressed in this

chapter are summarised to the best of the authors' understanding from the various participants’ Forum

contributions and should not be interpreted as the views of the ECB or the Eurosystem.

ECB Forum on Central Banking, November 2020

6

independence; and the role of fiscal policy in the post-COVID recovery. The papers,

presentations and video recordings of all sessions can be found at the ECB website.

2 Fundamental structural changes in the world economy:

“Slowbalisation” and climate change

One of the key structural changes in the world economy over the last decades was

globalisation. But since the Great Financial Crisis and with the rise of populism the

issue has emerged as to whether this process is reversing to de-globalisation. Based

on a plethora of data, Pol Antras (in Antras 2021) argues that international trade and

supply chains have slowed but not reversed ("slowbalisation") and may be regarded

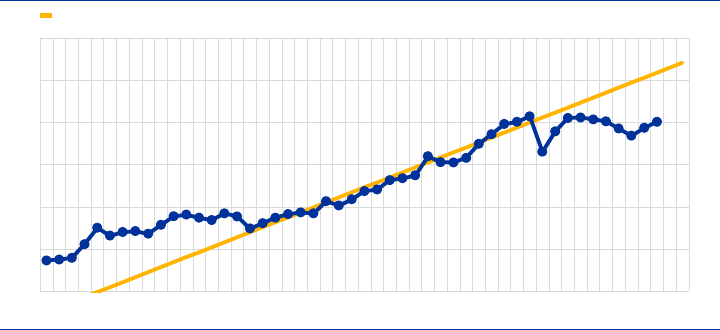

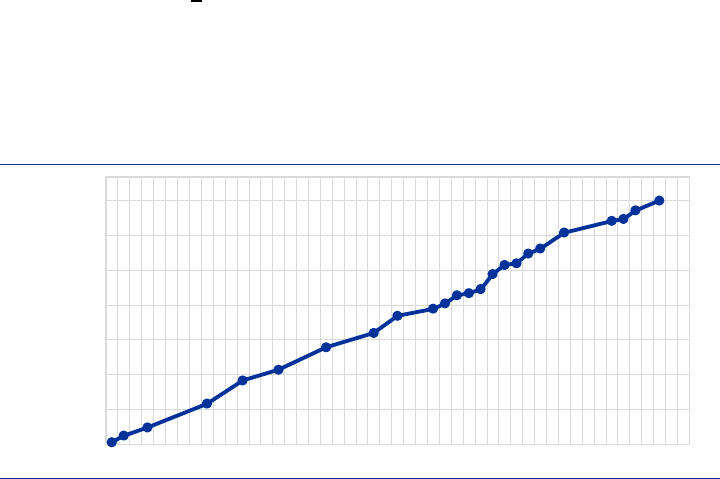

as not likely to turn to de-globalisation. The backward-looking part is illustrated in

Chart 1, which shows that after a period of very fast "hyperglobalisation" between the

mid-eighties and 2008, the share of world trade in world GDP has stayed roughly

constant.

Chart 1

World trade relative to world GDP (1970-2018)

Source: Antras (2021), based on World Bank’s World Development Indicators (link).

Note: Trade is defined as the sum of exports and imports of goods and services.

Looking forward, Antras argues that two out of three main factors that explained

"hyperglobalisation" are unlikely to reverse. First, new technologies will continue to

foster trade, as the case during the first Information and Communication Technology

(ICT) revolution, because those substituting (foreign) labour (such as robotisation or

3D printing) still generate increased demand for traded goods (such as machines or

IT parts). Second, the high sunk costs of establishing global supply chains make

them resilient to temporary shocks and make re-shoring only attractive for very

persistent shocks. The only hyperglobalisation factor risking to reverse is multilateral

trade liberalisation. So, in Antras' view the main challenges to globalisation are

political and institutional in nature. They can only be kept under control if

governments compensate the losers of globalisation better than they did in the past

(rather than resorting to protectionism).

10%

15%

20%

25%

30%

35%

40%

1970 1974 1978 1982 1986 1990 1994 1998 2002 2006 2010 2014 2018

Linear forecast based on 1986-2008 period

ECB Forum on Central Banking, November 2020

7

Susan Lund (in Lund 2021) added that China rotating from exports to domestic

consumption and building domestic supply chains can account for most of the global

trade slowdown over the last decade. As both reflect economic development, it may

be regarded as a positive story, one also other emerging economies may go through

in the future. Moreover, one should not forget that services trade grew much (about

80 per cent) faster than goods trade over a similar period. Lund, however, took a

somewhat different perspective on the resilience of global supply chains. Their

occasional disruption can have measurable implications for company profits and

therefore a large share of supply chain executives currently consider making them

safer, including through "near-shoring" and regionalisation.

Finally, Antras (2021) also discussed the impact of the COVID-19 pandemic on world

trade. His main conclusion was that, to the extent that economic agents perceive the

pandemic as a temporary shock (which has become more likely given the relatively

fast development of vaccines), the current crisis is unlikely to constitute a significant

de-globalisation force.

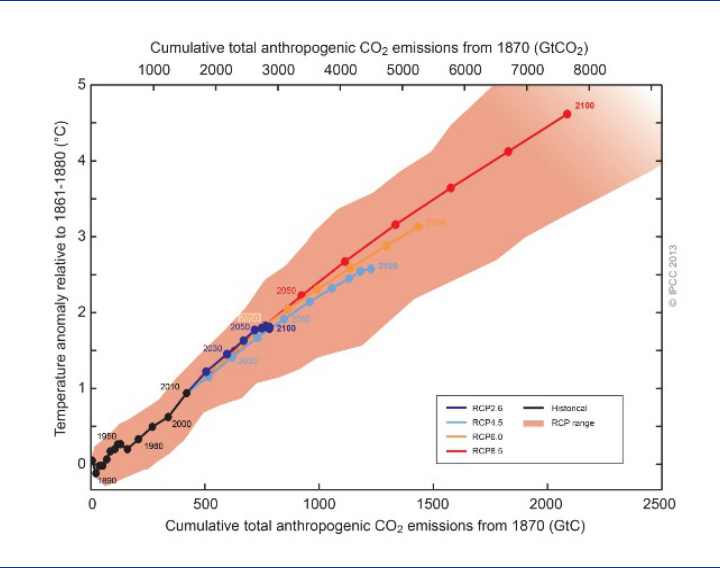

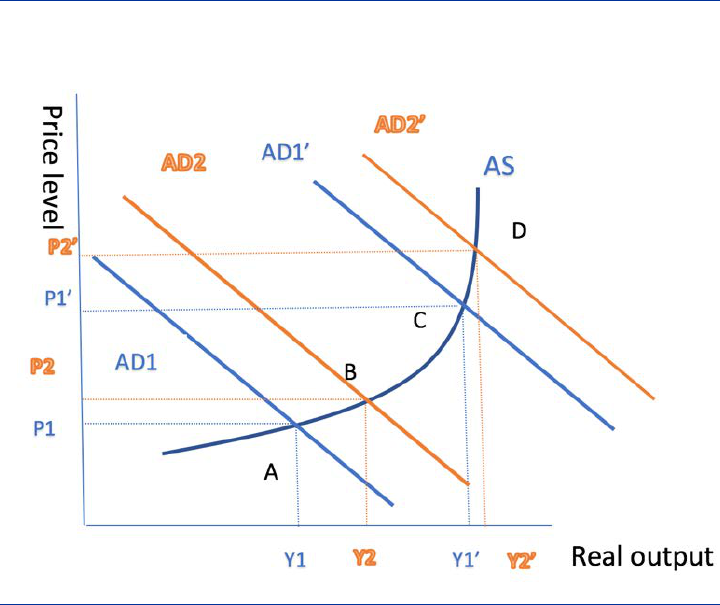

Climate change and the de-carbonisation that it requires is likely to set in motion

another set of major structural changes in the world economy, but Frederick van der

Ploeg (in van der Ploeg 2021) strongly warns that political logic involves the great

risk that too little is being done too late. This implies an unsmooth carbon transition

with financial market disruptions, stranded assets and financial instability. A sudden

shift in (expectations about) climate policy or a technological breakthrough can lead

to sudden changes in the market valuation of both carbon-intensive and carbon-

extensive firms (so-called tipping events).

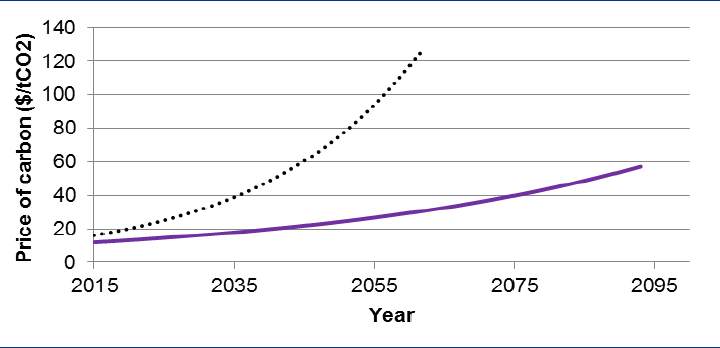

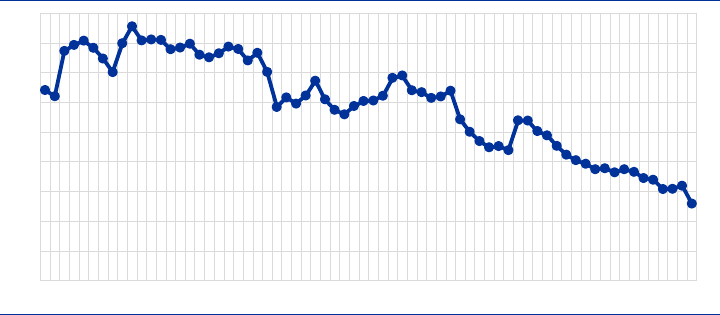

In his comprehensive survey paper, van der Ploeg first compares economists'

preferred Pigouvian approach of pricing carbon at its social costs (either via a carbon

tax or a system of tradable emission permits) with the route taken by the

Intergovernmental Panel on Climate Change (IPCC) of agreeing on a cap to global

warming. As illustrated in Chart 2 (taken from van der Ploeg 2018), the IPCC

approach would increase the carbon price (and therefore reduce carbon emissions

and increase renewables) much faster than standard Pigouvian approaches. The

Pigouvian approach doesn't take peak temperature constraints into account, and

thus prices don't have to rise so fiercely under it. In general, all these approaches

should not only curb the demand for fossil-fuel-based energy, but also stimulate

green research and development (R&D) and innovation, and speed up the move

towards a circular economy (in which resources are re-used rather than used up).

ECB Forum on Central Banking, November 2020

8

Chart 2

Evolution of the carbon price implied by the Pigouvian versus the carbon budget

approach to climate policy

Source: van der Ploeg (2018) and van der Ploeg (2021)

Note: The solid line represents the necessary evolution of the calibrated optimal carbon price, as derived from a simplified Dynamic

Integrated Climate-Economy (DICE, see e.g. Nordhaus 1993) model that sets the optimal price equal to the social cost of carbon

("Pigouvian approach"). The social cost is defined as the present discounted value of all future production losses stemming from

emitting one ton of carbon today. The dotted line not only takes into account the social cost of carbon but also the need to keep peak

global warming below 2 (relative to global temperature in the pre-industrial era; "carbon budget approach"). This is in line with the

route taken by the IPCC.

Among his many conclusions van der Ploeg (2021) calls for climate policies being

delegated to a politically independent emissions authority ("carbon central bank"),

the carbon price starting relatively high and then growing moderately but steadily

(avoiding paradoxical emission increases due to the anticipation of future policy

tightening), using revenues to compensate low-income households and to support

firms at risk from carbon-intensive imports, and using debt or transfers for

intergenerational fairness as well as keeping financial stability risks associated with a

disorderly transition under control with climate stress tests.

This stimulated a lively debate about the best institutional arrangements for

achieving timely decarbonisation. For example, Helene Rey wondered whether an

independent "carbon council" - as proposed in a recent Group of Thirty (2020) report

- could achieve net emissions neutrality by 2050 through targeting a carbon price

path and giving forward guidance in some analogy to independent central bank

monetary policy. Harald Uhlig cautioned not to overstretch delegation from

governments and parliaments to expert committees when re-distributional effects

induce some people to lose their jobs and some companies to go bankrupt. Lucrezia

Reichlin recalled that such active climate policies would still need much improved

and mandatory data standards and disclosure. Signe Krogstrup (in Krogstrup 2021)

wondered how one gets from van der Ploeg's literature overview suggesting that

climate risks are increasingly priced in financial markets to the under-pricing of risk

justifying policy intervention. In what concerns the role of central banks, Francois

Villeroy de Galhau suggested that central banks can look at whether climate risks

are adequately reflected in their collateral frameworks. Krogstrup concluded though

that fiscal policy should be first in line for a cost-efficient carbon transition, but central

banks will address their stake in it.

ECB Forum on Central Banking, November 2020

9

3 Formulations of central banks' inflation aim close to the

effective lower bound of nominal interest rates

One of the key challenges for monetary policy in our times is the sustained

downward trend in natural interest rates that can be estimated for the past decades

(see, e.g., Laubach and Williams 2003 on estimating the natural interest rate and

Brand et al. 2018 for euro area evidence). The low estimates of natural rates imply

that central banks' conventional interest rate policy may not be able to provide

sufficient stimulus in the presence of negative shocks, as policy rates cannot be

reduced low enough below the natural rate. This well-known problem gave rise to an

active discussion about the formulation of the ECB's inflation aim in its monetary

policy strategy.

In line with much of the New-Keynesian literature, Klaus Adam (in Adam 2021)

argued that an increase in the inflation target could be a solution, because - if the

increase is credible - the inflation expectations that it would induce would stimulate

the economy through lower real interest rates. But his research suggests that the

declining natural rate also influences asset price volatility and that therefore the

efficiency of financial markets has a bearing on the extent to which the target should

be increased and whether monetary policy should react to longer run asset price

fluctuations.

The New-Keynesian model developed in Adam et al. (2020) exhibits a negative

relationship between the natural rate and asset price volatility, as a lower discount

rate amplifies the present value changes of prices in response to future expected

pay-off changes. This relationship becomes more pronounced for inefficient

subjective price expectations (forecast errors are corrected sluggishly), as observed

in surveys, and therefore influences the level of the optimal inflation target. With

rational expectations in financial markets the optimal increase in the target to

compensate for the constrained policy rate is relatively small in the model. When

subjective expectations create procyclical asset price fluctuations, however, the

inflation target needs to be increased by much more, as the increased financial

volatility drives the economy more frequently towards the effective lower bound of

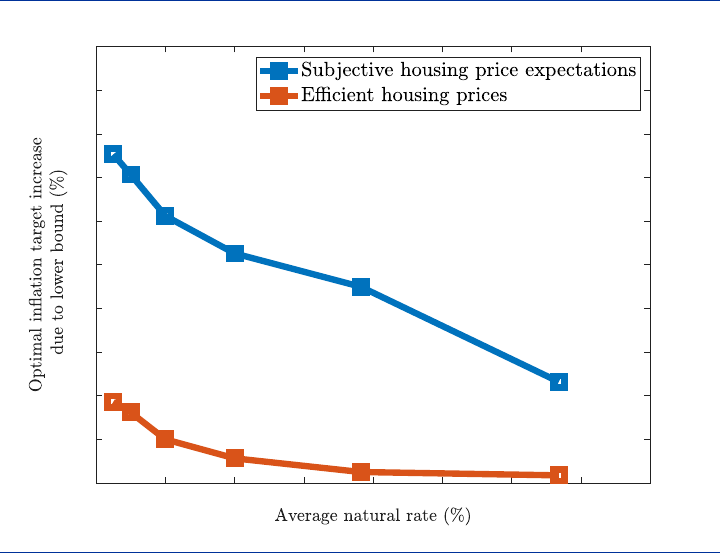

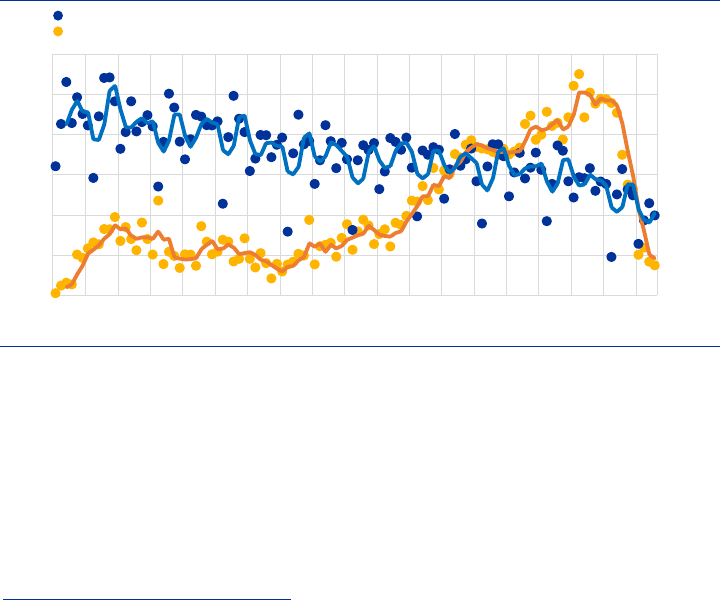

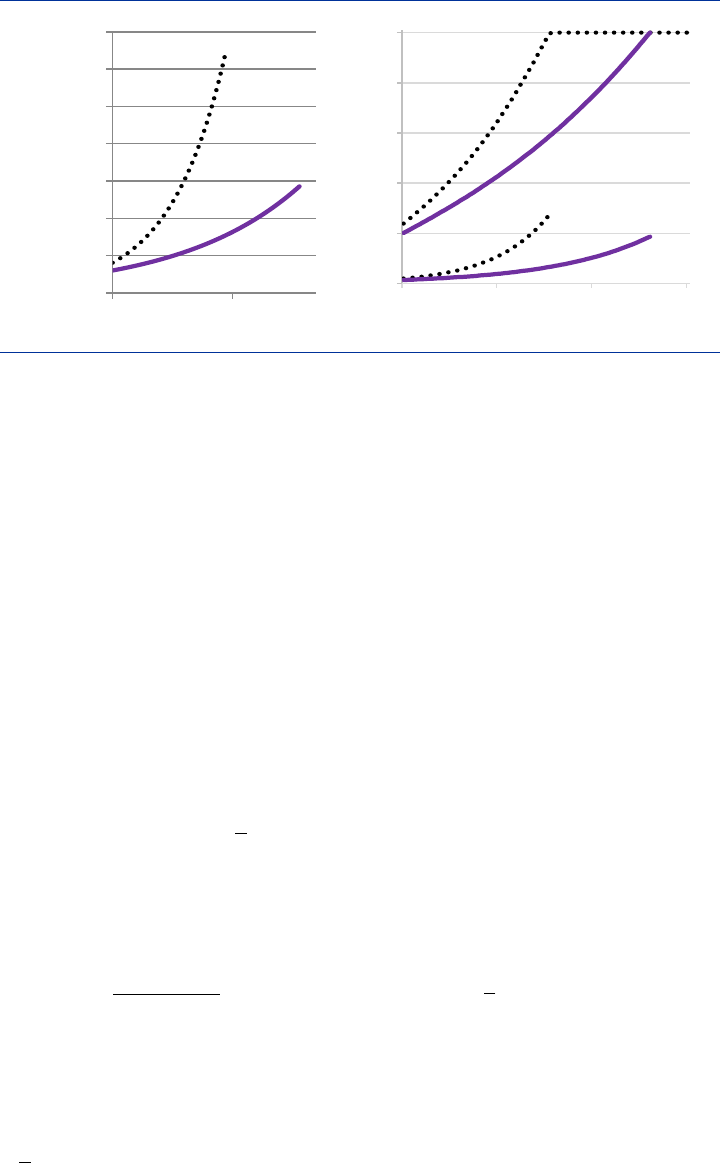

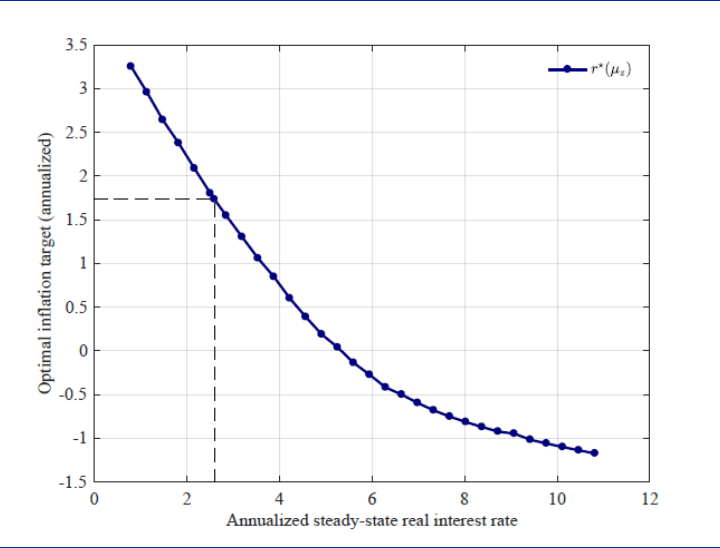

nominal interest rates (ELB). Chart 3 shows the optimal inflation targets (vertical

axis) derived from the model (calibrated to the US economy) for different levels of

the natural rate (horizontal axis) and depending on whether asset price volatility is

efficient (red line) or subject to procyclical adaptive behaviour emerging from

subjective expectations (blue line).

ECB Forum on Central Banking, November 2020

10

Chart 3

Relationships between the optimal inflation target, the natural rate of interest and

expectation formation in housing markets due to the effective lower bound on

nominal rates

Source: Adam (2021)

Note: This chart illustrates the optimal inflation target, i.e., the average inflation outcome under optimal conduct of monetary policy. For

each considered level of the average natural rate (on the x-axis), the chart reports the optimal inflation target (on the y-axis) in an

economy with an effective lower bound constraint, relative to the target that would be optimal in the absence of a lower-bound

constraint. The blue line shows the optimal inflation target in an economy where house prices are efficient (i.e. driven by fundamentals

only). The red line reports the optimal inflation target for the case where housing prices are driven – at least partly – by fluctuations in

subjective housing price expectations. Numbers are based on a New Keynesian sticky price model from Adam, Pfaeuti and Reinelt

(2020), calibrated to US data. In the absence of a lower bound constraint, the optimal inflation target is zero, because the model

abstracts from other forces that make targeting positive average rates of inflation optimal.

Interestingly, in this model the central bank finds "leaning" against inefficient asset

price fluctuations optimal, undershooting the inflation target in upturns and

overshooting it in downturns. The reason is that inefficiently high asset price volatility

has too high a welfare cost in terms of capital misallocation towards appreciating

assets.

In her discussion, Argia Sbordone (in Sbordone 2021) argued that, in Adam's model,

the increased incidence of the lower bound constraint does not imply that optimal

policy raises the long-term inflation target. Instead, it increases the number of

periods for which the central bank should temporarily target higher future inflation

than its stated long-term inflation target. This de facto would be similar to average

inflation targeting (AIT), the policy announced by the US Federal Reserve in 2020.

AIT makes up for past shortfalls in inflation relative to target through future inflation

that is temporarily in excess of the target. In Sbordone's view such a policy is

preferable, because it faces a lower risk of permanently higher inflation when ELB

incidences turn out to be infrequent. Alan Blinder made the point, however, that the

vague formulation by the Fed risked undermining the basic idea of AIT. Finally,

Sbordone pointed out that Adam's result about the optimality of "leaning against the

0 0.5 1 1.5 2 2.5 3 3.5 4

0

0.2

0.4

0.6

0.8

1

1.2

1.4

1.6

1.8

2

ECB Forum on Central Banking, November 2020

11

wind" is robust to various extensions of the model. In the context of the final panel of

central bank leaders, Federal Reserve Chairman Jerome Powell mentioned that the

Board of Governors took away from the fact that the 30-year long decline in inflation

and interest rates had contributed to financial imbalances and crises a very strong

focus on financial stability, as witnessed by its financial stability report published

since 2018.

In the first panel discussion Jordi Galí (in Galí 2021, Chart 1) showed a similar

negative relationship as Adam between the natural rate and the central bank's

optimal inflation target, based on a New-Keynesian model calibrated to euro area

data (Andrade et al. 2021). It suggests that while a target between 1.5 and 2 per cent

would be optimal for a steady-state real interest rate between 2 and 3 per cent, for

the lower equilibrium rate levels estimated nowadays the target could easily increase

to levels around 3 per cent. However, for increasingly aggressive monetary policy

rules embodying an AIT with rising averaging window to 4 or even 8 years, the

optimal target could be reduced to close to 2 per cent. Aggressive countercyclical

fiscal policy rules (e.g. emergency policies around 4 per cent of GDP in deep

recessions) would have a similar effect in the model. Galí concluded that rather than

deciding in favour of one of the three options, policy makers may want to pursue all

the three at the same time (although central banks can only control the first two).

Contributing additional perspectives to the discussion, Volker Wieland (in Wieland

2021) reached somewhat different conclusions. First, comparing average inflation

outcomes for the Harmonised Index of Consumer Prices (HICP, the ECB's headline

inflation indicator), the GDP Deflator and the Import Price Deflator, he argued that

the low inflation during the recovery after the European sovereign debt crisis seemed

to be mainly driven by import prices, which are hard to influence with monetary

policy, whereas the GDP deflator drifted towards levels above 2 per cent. Second,

the HICP does not capture owner-occupied housing, a category experiencing

significant price increases in some euro area countries. He therefore recommended

that the ECB would broaden the range of measures considered for its inflation

assessments. Next he presented elements of a model of optimal monetary policy in

which the effectiveness of unconventional monetary policies, such as quantitative

easing (QE), is subject to uncertainty and their adoption would have some

unintended side effects with welfare costs (Wieland 2020). Both considerations

would argue in favour of optimal monetary policies close to the ELB driving inflation

towards target more slowly rather than more aggressively, as e.g. suggested in the

AIT literature.

Overall, Wieland regarded it as problematic to raise the ECB's inflation aim at a time

when inflation is very low, as the distance between the two is very large in such a

situation and it would require further policy easing. If such easing is difficult to

achieve, the desired inflation expectations effect of a higher target may not

materialise and trust in the central bank’s ability to reach the target might be eroded.

In the general discussion, Vítor Constâncio and Ignazio Visco argued the other way

around, worrying that too little ambition could contribute to de-anchoring inflation

expectations making convergence to the desirable levels of inflation more difficult.

Yannis Stornaras wondered whether at the ELB expansionary fiscal policy was not

ECB Forum on Central Banking, November 2020

12

preferable to raising the inflation target. Adam and Galí recognised the challenge but

preferred to address it by revising the inflation target in smaller steps over time (e.g.

through regular reviews) and increasing it ("opportunistically") by more when inflation

has reached higher levels. Fabio Panetta drew from the discussion that central

banks have less conventional policy space for low inflation than for high inflation and

therefore have to act less tolerantly to inflation drifting below target.

4 Formal versus informal monetary policy communication

Annette Vissing-Jorgensen opened the topic of communication approaches for a

central bank's monetary policy strategy in her panel discussion (Vissing-Jorgensen

2021). While formal, public and on-the-record communications are a key and

unambiguously positive part of monetary policy making, ensuring its effectiveness

and accountability, the same does not apply to informal, off-the-record and

unattributed communications. And an academic literature using data for the United

States suggests that such informal communications - between meetings of the

Federal Open Market Committee - can have material effects on stock market returns.

Vissing-Jorgensen focused particularly on unattributed communications, such as

"sources stories" disseminated by the media. She recognised some benefits of such

informal communication if it is done institutionally, as non-attribution may preserve

more flexibility for policy makers, avoid time-consuming and potentially controversial

public debates and allow gauging outside views on different policy options. But she

regarded unattributed individual communication, driven by disagreements among

policy makers, as subject to a prisoner's dilemma-type problem and unambiguously

detrimental. She illustrated this point with a game-theoretic model of individual policy

makers trying to "spin" market expectations towards their preferred choices (Vissing-

Jorgensen 2020). While asset prices may not be distorted on average, as victories

and defeats cancel out over time, the policy space of the decision-making body will

still be constrained, as central banks have to mind about too frequent or large

deviations between market expectations and ultimate decisions. Apart from

discouraging individual unattributed communication, Vissing-Jorgensen

recommended consensus-building approaches for central bank governors, as they

would naturally reduce incentives for their committee members to engage in such

individual informal communications.

5 Monetary policy, the allocation of risk and central bank

independence

In the second panel discussion Lucrezia Reichlin (in Reichlin 2021) spelled out a

conceptual framework for the relationships between monetary policy, risk and

financial stability in the new world of unconventional instruments. Distinguishing what

she called "passive" instruments, such as long-term refinancing operations, which

act as complements to standard interest rate policy, from "active" instruments, such

as quantitative easing asset purchases, acting as substitutes for rate policy at the

ECB Forum on Central Banking, November 2020

13

ELB, she stressed the multi-dimensional use of the various instruments, which have

to be thought of as "packages" controlling the entire yield curve and creating

complex interactions between macroeconomic and financial risks.

These policies can only be effective in supporting the macroeconomy, if they induce

the creation of new assets climbing up the risk spectrum. If the new assets finance

productive activities, then the additional risks are "good". But prudential policy would

need to prevent the creation of "bad" risks. Delayed, partial or incoherent use of the

range of instruments would undermine effectiveness; and so would be neglecting

interactions and coordination with fiscal policy. In response to a question by Beatrice

Weder di Mauro, Reichlin emphasised the additional communication needs for

making the logic of the complex new instrument combinations and the

complementarities involved understood.

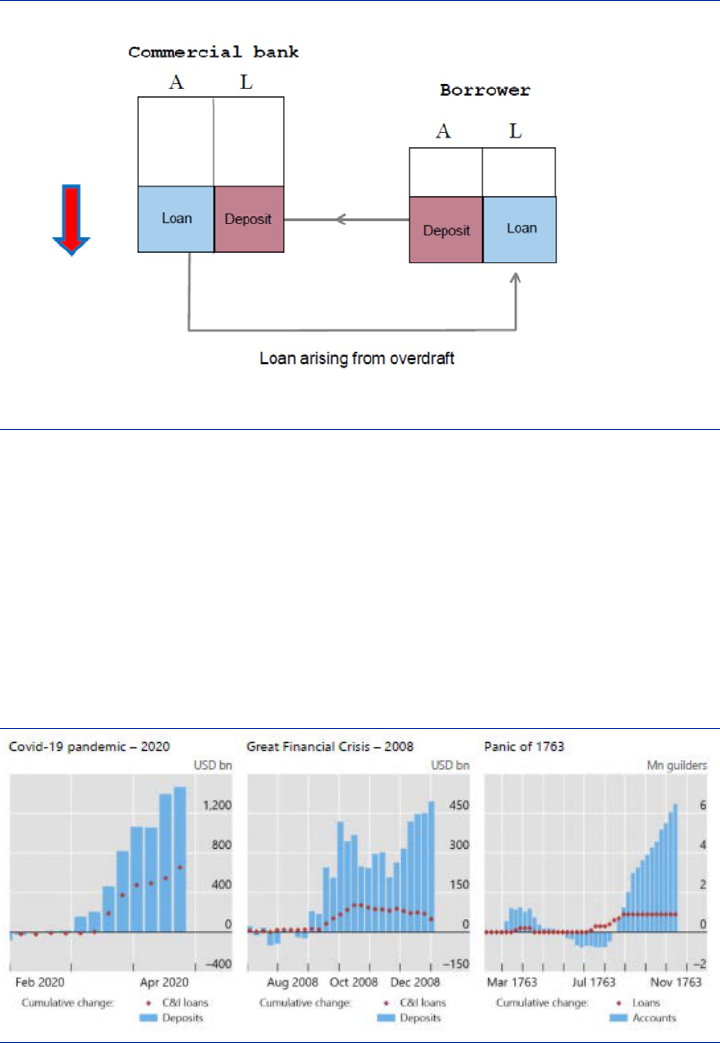

Hyun Shin (in Shin 2021) complemented this with emphasising the great importance

of "elastic nodes" in the financial system. In situations of stress, these elastic nodes

would flexibly accommodate the much-increased demand for money and thereby

help restore stability. The first line of defence should be well-capitalised and resilient

commercial banks; an example being how US banks increased commercial and

industrial loans during the "dash for cash" in March 2020, when the COVID crisis had

broken out, by allowing companies to draw on their credit lines. (In fact, several

Forum speakers - such as Jerome Powell and Bank of England Governor Andrew

Bailey - confirmed that banks generally stood up to this first major test of the reforms

introduced after the Great Financial Crisis.) Such elastic nodes are not new though,

as for example the strong deposit creation of the Bank of Amsterdam - an early

predecessor of central banks - through the acceptance of coins and bullion during

the crisis of 1763 illustrates (e.g. Schnabel and Shin 2004).

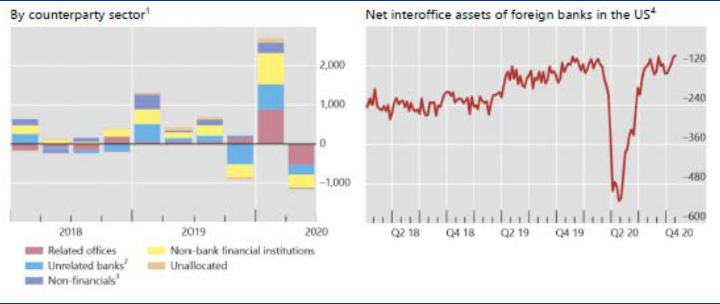

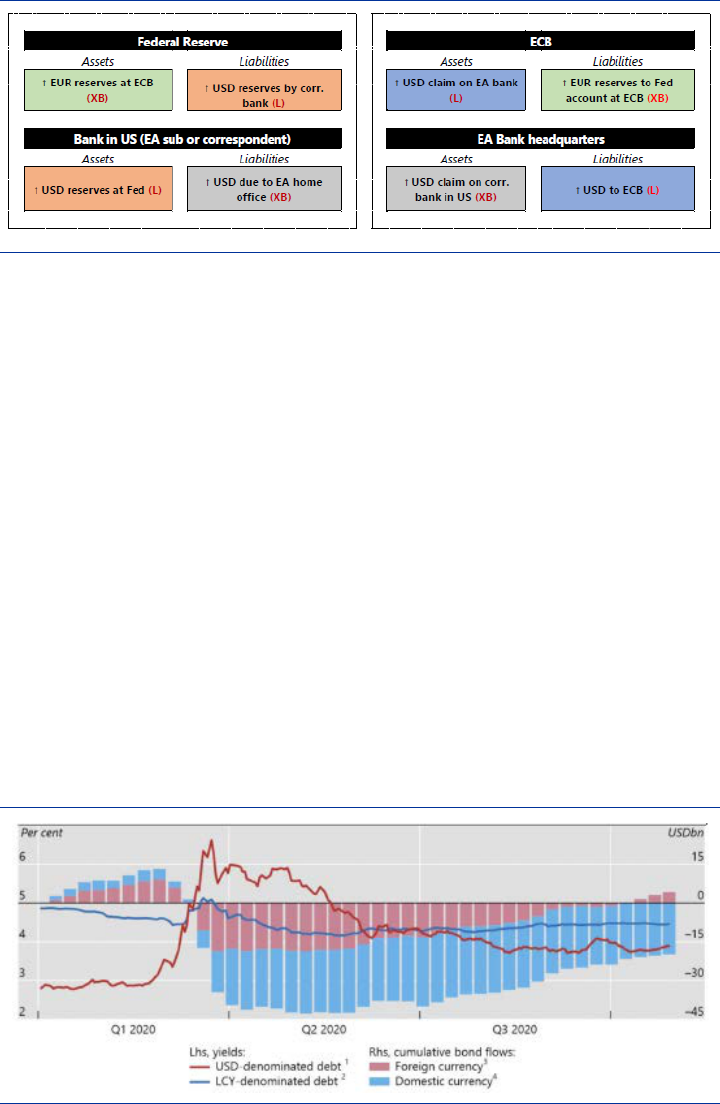

A third example of elastic nodes in the international arena is the circular flow of US

dollars between the Federal Reserve, the ECB, European and US-based banks

enabled through central bank swap lines. Its operation could be seen through a large

increase of cross-border interbank positions broadly matching the swap amounts

during the first quarter of 2020. So, central banks would constitute the second line of

defence, for example through facilities that Reichlin had included in her first category

of instruments complementary to conventional interest rate policy.

Markus Brunnermeier (in Brunnermeier 2021) broadened the discussion with a

proposal about how a monetary policy strategy can be robustified against the risk of

a central bank getting trapped in high inflation or deflation. At the time of the Forum

the main problem was still very low inflation. But in the post-COVID recovery an

"inflation whipsaw" could emerge, in that pent-up demand, government commitments

or capital re-allocation could create a reversal to high inflation (Brunnermeier et al.

2020). In other words, it is necessary that the central bank can "put on the breaks"

later, in order to be able to confidently stimulate the economy with force in the low

inflation context.

But if during the downturn government debt becomes too high, a situation of fiscal

dominance could occur, as the central bank could not raise interest rates in the

upturn without destabilising the budgets. Similarly, if the banking sector was not to

ECB Forum on Central Banking, November 2020

14

maintain its resilience and if the government was unwilling or unable to recapitalise

the banks, the central bank may be forced to stabilise them with monetary policy

redistributing risk - a situation of financial dominance.

Brunnermeier proposed that these tail risks, together with some other robustness

checks, would be considered in a re-oriented second pillar in the ECB's monetary

policy strategy. This would institutionalise heterogeneous thinking and go against

relying on a uniform class of economic models. Against fiscal dominance he

suggested to strengthen the central bank's independence through increasing its

equity capital. Against financial dominance Brunnermeier advocated adequate

prudential supervision and to design unconventional monetary policies in a way that

would not promote too much leverage in the financial and corporate sectors.

Paul de Grauwe challenged Brunnermeier on the need for re-capitalisations, as the

central bank can run monetary policy with negative equity and the creation of

additional central bank equity would not have any material macroeconomic

implications. Brunnermeier and Shin retorted, however, that there are limits for how

negative the central bank can go without the public's trust in the currency being

eroded (see also Hall and Reis 2015). Reichlin agreed and added that also the way

how seigniorage is distributed to treasuries may be relevant and it may be wise to

have some principles about that in the Eurosystem.

6 The role of fiscal policy in the post-COVID recovery

Evi Pappa (in Pappa 2021) made a strong plea for discretionary fiscal policy taking a

prominent role in the recovery from the COVID pandemic, notably through

government investment. The theoretical case relies on higher fiscal multipliers in a

situation in which conventional monetary policy is close to the ELB, as the central

bank would not tighten in response to inflation expectations ensuing from the fiscal

stimulus. In line with this, Christine Lagarde argued in her introductory speech to the

Forum (Lagarde 2021) that monetary policy should minimise any crowding out

effects on private investment that may emerge from rising market interest rates that

the fiscal expansion could induce.

Based on the experiences with European Union structural funds for member states

and regions over the last 30 years (see Canova and Pappa 2020, using a local

projections methodology), Pappa particularly supported public investment spending

funded by the Next Generation EU recovery programme (Table 1). For example,

grants provided by the European Regional Development Fund (ERDF), which aims

to foster investments in innovation and research, to foster the digital agenda, and to

support small and medium-sized enterprises, are found to have sizeable short-term

effects (over one year) on growth, investment, employment, productivity, and real

wages, making them particularly useful for rapid countercyclical policies. Measurable

effects of grants by the European Social Fund (ESF), whose aim it is to support

investments in education and health, and to fight poverty, take more time to

materialise (about three years). While these results mask strong cross-country

heterogeneity, countries like Finland, France, Italy, Latvia, Romania and Spain seem

ECB Forum on Central Banking, November 2020

15

to be systematically benefiting from the two funds in terms of growth and

employment. Accordingly, Lagarde (2021) called for the Next Generation EU

package to become operational without delay.

Table 1

Average cumulative multipliers from grants under the European Regional

Development Fund (ERDF) and the European Social Fund (ESF)

Macroeconomic

variables ERDF funds ESF funds

1 year 2 years 3 years 1 year 2 years 3 years

Gross value added

2.42

(0.19)

1.56

(0.32)

0.56

(0.32)

-0.14

(0.63)

2.70

(0.79)

5.05

(0.82)

Employment

0.86

(0.15)

-0.03

(0.27)

-0.42

(0.29)

-0.33

(0.23)

-0.62

(0.34)

0.96

(0.36)

Investment

8.07

(1.71)

0.53

(2.68)

-1.40

(2.69)

2.13

(1.65)

2.75

(1.63)

3.58

(1.88)

Labour

productivity

3.66

(0.37)

-3.65

(0.78)

-4.45

(0.75)

4.09

(0.70)

0.22

(0.83)

3.26

(0.85)

Real

Compensation

3.85

(0.36)

-2.62

(0.85)

-4.50

(0.84)

2.95

(0.32)

-1.54

(0.62)

4.54

(0.69)

Source: Canova and Pappa (2020)

Notes: This table examines the dynamic effects of ERDF and ESF grants on regional (NUTS3-level) macroeconomic variables in

European Union countries, using local projections. The main regression specification is as follows: y

,,

= a

,

+ b

,

y

,,

+ c

,

x

,,

+

e

,,

,where y

,,

is the cumulative growth of the macroeconomic variable of interest in region i and year t over the time-horizon h (either

1,2 or 3 years, see columns) and x

,,

is the cumulative change in the relevant grant (scaled by regional gross-value added). The

estimated coefficients displayed in the table correspond to c

,

and standard errors are in parentheses. The coefficients can therefore

be interpreted as the cumulative fiscal multipliers of the fund grants (euro change per euro of grants), or put differently as elasticities

measured in per cent, at each horizon h. Given the potential endogeneity of structural funds to EU economic conditions, the authors

instrument actual grants with their "innovations". To this effect they run the following auxiliary regression: x

,,

=

,

+

,

w

,

+ u

,,

,

where w

,

represents a set of four aggregate euro area variables: GDP, employment, the GDP deflator, the nominal interest rate, and

the nominal effective exchange rate. They then use the "innovation" u

,,

as an instrument for x

,,

in the main equation.

At the same time, Pappa cautioned that the literature suggests that the size of fiscal

multipliers can depend on many factors. For example, high public debt, low

confidence and economic uncertainty could reduce them or, in extreme cases, turn

them negative. While endorsing the proposals of the European Fiscal Board (2019)

for reforming the Stability and Growth Pact, she made the "daring suggestion" that

public debt restructurings in Europe may substantially ease the road to recovery (see

also Corsetti et al. 2016).

Vítor Gaspar (in Gaspar 2021) added that while national fiscal support packages

increased euro area public debt by about 17 percentage points during 2020 to above

100 per cent of GDP, the primary risk at the time of the Forum was the premature

withdrawal of fiscal support. Moreover, he joined Evi Pappa in supporting public

investment via the Next Generation EU programme, emphasising the International

Monetary Fund's assessment that fiscal multipliers are particularly elevated in

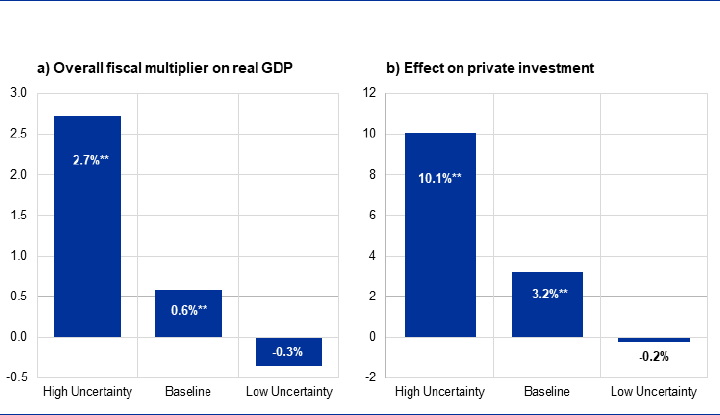

periods of high uncertainty (see Chart 5, based on IMF 2020), such as the case

during the COVID-19 pandemic (e.g. Barrero and Bloom 2020). According to Gaspar,

this happens because public support to investment in green and digital technologies

would facilitate and give confidence to private firms to invest, in part because public

investments signal governments' commitment to sustainable growth.

ECB Forum on Central Banking, November 2020

16

Chart 5

Public investment multipliers and private investment "crowd-in" for different levels of

economic uncertainty

Cumulative two-year-ahead macroeconomic effects of a one-percent-of-GDP unexpected

increase of public investment

Source: Gaspar (2021) and IMF Fiscal Monitor (October 2020)

Note: Effects on the vertical axes are measured in percentage changes. Results are based on local projection estimations using the

model y

,

y

,

=

+

+

G

,

FE

,

+

1 G

,

FE

,

+

,

+

,

, where y

,

is the log of the macroeconomic variable of

interest (real GDP for panel a) and private investment for panel b) for country i in year t, FE

,

is a positive unexpected shock to public

investment spending (as share of GDP), in deviation from IMF forecasts, z is an indicator of the degree of uncertainty, and G

,

is the

corresponding smooth transition function between different levels of uncertainty. M

,

includes lagged GDP growth and lagged shocks.

Uncertainty is measured by the standard deviation of GDP growth rate forecasts across professional forecasters as published by

Consensus Economics, using for each year the spring vintage of the forecasts. Data covers 72 advanced and emerging markets; the

sample period is 1994-2019.

The nuanced difference between Pappa and Gaspar on the role of uncertainty gave

rise to a discussion about which conditions would have to be fulfilled so that

multipliers remain positive (and potentially large) and the scope for multiple

equilibriums be reduced (as raised e.g. by Giancarlo Corsetti). Gaspar emphasised

investments in high-quality projects, high standards of transparency and governance

in infrastructure investments and a robust approach to public debt management.

Daniel Gros wondered whether containing uncertainty would not require addressing

public debt levels. Pappa mentioned the reduction of implementation lags, although

there could be a trade-off with quality. Moreover, the relative roles of fiscal and

monetary policy should be clearly communicated.

In her introductory speech, Christine Lagarde (in Lagarde 2021) had pointed out that

in a pandemic emergency, when interest rates are already very low, private demand

is constrained by health containment measures and levels of economic uncertainty

are very high, fiscal policy can be particularly effective for at least two more reasons.

First, it can support the sectors most affected in a more targeted way than monetary

policy (see also Woodford 2020). Second, as fiscal policy determines about half of

total spending in the euro area, it can help coordinate the other half, breaking

"paradox of thrift" dynamics in the private sector and thereby also reinvigorating the

transmission of monetary policy. All in all, the right policy mix requires that fiscal

policy remains at the centre of the stabilisation effort. At the same time, many Forum

speakers highlighted the unprecedented levels of uncertainty that the COVID

pandemic had generated and the challenges that it implied for the recovery. For

example, Andrew Bailey mentioned that relevant uncertainty measures reached

ECB Forum on Central Banking, November 2020

17

during 2020 their highest levels since a quarter of a century, making this feature the

most frightening aspect of the pandemic from an economic policy perspective.

References

Adam, K. (2021), “Monetary policy changes from falling natural interest rates”, in this

volume.

Adam, K., Marcet A., and Beutel, J. (2017), “Stock price booms and expected capital

gains”, American Economic Review, Vol. 107, pp. 2352-2408.

Adam, K., Pfaeuti, O. and Reinelt, Z. (2020), “Falling natural rates, rising housing

volatility and the optimal inflation target”, CRC TR 224 Discussion Paper, No. 235,

November.

Andrade, P., Galí, J., Le Bihan, H., and Matheron, J. (2021), "Should the ECB

Revise its Strategy in the Face of a Lower r*," mimeo., Pompeu Fabra University,

January.

Antras, P. (2021), “De-globalisation? Global value chains in the post-Covid-19 era”,

in this volume.

Attig, D., Baker, S., Barrero, J. M., Bloom, N., Bunn, P., Chen, S., Davis, S. J.,

Leather, J., Meyer, B., Mihaylov, E., Mizen, P., Parker, N., Renault, T., Smietanka, P.,

Thwaites, G. (2020), “Economic uncertainty before and during the COVID-19

pandemic,” Journal of Public Economics, Vol. 191, 104274.

Barrero, J. and Bloom, N. (2020), “Economic uncertainty and the recovery,” in

"Navigating the Decade Ahead: Implications for Monetary Policy", Federal Reserve

Bank of Kansas City, Economic Policy Symposium Proceedings, pp. 255-284.

Brand, C., Bielecki, M., and Penalver, A. (2018), “The natural rate of interest:

estimates, drivers, and challenges to monetary policy”, ECB Occasional Paper

Series, No 217, December.

Brunnermeier, M. (2021), “De- and inflationary traps: strengthening ECB’s second

pillar to avoid fiscal and financial dominance”, in this volume.

Brunnermeier, M., Merkel, S., Payne, J., and Sannikov, Y. (2020), COVID-19:

inflation and deflation pressures, mimeo., Princeton University, September.

Canova, F., and Pappa, E. (2021), “What are the likely macroeconomic effects of the

EU Recovery plan?”, mimeo., Pompeu Fabra UniversityFebruary.

Corsetti, G., Dedola, L., Jarocinski, M., Mackowiak, B. and Schmidt, S. (2016).

Marcoeconomic stabilization, monetary-fiscal interactions and Europe's monetary

union. ECB Working Paper Series, No 1988, December.

European Fiscal Board (2019), “Assessment of EU fiscal rules with a focus on the six

and two-pack legislation”. September 1.

ECB Forum on Central Banking, November 2020

18

Gali, J. (2021), “The decline in r* and the ECB strategy”, in this volume.

Gaspar, V. (2021), “Discussion of Evi Pappa’s “Fiscal rules, policy and

macroeconomic stabilization in the euro area””, in this volume.

Greenwood, R., and Shleifer, A., (2014), “Expectations of returns and expected

returns”, Review of Financial Studies, Vol. 27, pp. 714–746.

Group of Thirty (2020), "Mainstreaming the transition to a net-zero economy",

Washington (DC), October.

Hall, R., and Reis, R. (2015), "Maintaining central-bank financial stability under new-

style central banking ", mimeo., Stanford University, 16 July.

IMF (2020), Fiscal monitor: policies for the recovery, International Monetary Fund,

Washington. https://www.imf.org/en/publications/fm/issues/2020/09/30/october-2020-

fiscal-monitor.

Krogstrup, S. (2021), “Discussion of “Macro-financial implications of climate change

and the carbon transmission” by Frederick van der Ploeg”, in this volume.

Lagarde, C. (2021), "Monetary policy in a pandemic emergency", in this volume.

Laubach, T., and Williams, J. C. (2003). Measuring the natural rate of interest.

Review of Economics and Statistics, 85(4), pp. 1063-1070.

Lund, S. (2021), “De-globalisation? The recent slowdown of global trade and

prospects for future rebalancing”, in this volume.

Nordhaus, W. D. (1993), "Optimal greenhouse-gas reductions and tax policy in the

'DICE' model", American Economic Review, Vol. 83, pp. 313-317.

Pappa, E., (2021), “Fiscal rules, policy and macroeconomic stabilization in the euro

area”, in this volume.

Reichlin, L. (2021), “Non-standard monetary policy instruments: effectiveness and

risks”, in this volume.

Sbordone, A. (2021), “Discussion of “Monetary policy challenges from falling natural

interest rates” by Klaus Adam”, in this volume.

Shin, H.S. (2021), “Central bank balance sheets and financial stability”, in this

volume.

Schnabel, I., and Shin, H.S. (2004), "Liquidity and contagion: the crisis of 1763",

Journal of the European Economic Association, Vol. 2, pp. 929-968.

van der Ploeg, F. (2018), “The safe carbon budget”, Climate Change, Vol. 147, pp.

47-59.

van der Ploeg, F. (2021), “Macro-financial implications of climate change and the

carbon transmission”, in this volume.

ECB Forum on Central Banking, November 2020

19

Vissing-Jorgensen, A. (2020), " Central banking with many voices: the

communications arms race", mimeo., University of California at Berkeley, 2 February.

Vissing-Jorgensen, A. (2021), "Informal central bank communication", in this volume.

Wieland, V. (2020), “Quantitative easing: the proportionality principle and Brainard-

style policy attenuation”, unpublished manuscript., University of Frankfurt.

Wieland, V. (2021), “The decline in euro area inflation and the choice of policy

strategy”, in this volume.

ECB Forum on Central Banking, November 2020

20

Monetary policy in a pandemic

emergency

Introductory speech by Christine Lagarde

1

1 Introduction

Let me begin by welcoming all of you to this year’s ECB Forum on Central Banking.

Regrettably, we cannot be together in Sintra this time, but I trust that this virtual

environment will be no less conducive to challenging ideas and productive debate.

The purpose of this year’s conference is to examine the challenges facing central

banking in a shifting world. We will be discussing many of the long-term trends

monetary policy has to contend with, including shifting patterns of globalisation,

climate change and a lower natural interest rate.

Actually, the largest shift central banks are facing today may well turn out to be the

pandemic itself. As John Kenneth Galbraith said, “the enemy of the conventional

wisdom is not ideas, but the march of events”. And the events we are seeing today

are momentous.

The coronavirus (COVID-19) has produced a highly unusual recession and is likely

to give rise to a similarly unsteady recovery. Today I would like to talk about how the

ECB’s monetary policy has responded to this unique environment, and how we can

best contribute to supporting the economy going forward.

2 A highly unusual recession

The deliberate shutdown of the economy triggered by the COVID-19 pandemic has

produced a highly unusual recession. Most importantly, it has infiltrated and crippled

sectors that are normally less sensitive to the economic cycle. In a regular recession,

manufacturing and construction are typically hit harder by the cyclical downturn,

while services are more resilient. But during the lockdown in the spring, we saw the

reverse.

Compare our experience in the first half of this year with the first six months following

the Lehman crash. After Lehman, manufacturing contributed 2.8 percentage points

to the recession and services contributed 1.7 percentage points. But this year, the

loss was 9.8 percentage points for services and much less, 3.2 percentage points,

for manufacturing.

1

President of the European Central bank

ECB Forum on Central Banking, November 2020

21

This has three important implications.

First, research finds that the recovery from a services-led recession tends to be

slower than from a durable goods-led recession, as services create less pent-up

demand than consumer goods.

2

For example, people are unlikely to take twice as

many holidays abroad next year to compensate for their lack of foreign travel this

year.

Second, as services are more labour-intensive, services-led recessions have an

outsized effect on jobs. Five million people in the euro area lost their jobs in the first

half of this year. Of those, almost half worked in retail and wholesale trade,

accommodation and food services, and transportation, despite these activities

representing less than one-fifth of output. In the six months after Lehman, the worst

affected sector – industry – suffered only 900,000 job losses.

And third, these job losses hurt socio-economic groups unevenly. In the first half of

2020, the labour force contracted by almost 7% for people with low skills – who

typically also have lower incomes – while it fell by 5.4% for those with medium skills

and rose by 3.3% for those with high skills. This is double the loss of low-skilled jobs

we saw in the six months after Lehman.

In addition to their social impact, job losses for people with lower incomes present a

particular threat to the economy, because around half of those at the bottom of the

income scale face liquidity constraints and therefore consume more of their

income.

3

The labour-intensity of the worst-hit sectors also heightens the risk of

hysteresis and “scarring” in the labour market.

While job retention schemes have played a key role in mitigating these risks, they

could not eliminate them entirely. Even though many workers quickly returned to

regular employment once restrictions were lifted, a large number of people who lost

their jobs in the spring left the labour force and stopped looking for work, with 3.2

million workers classified as “discouraged”. This is so far different from the post-

Lehman period, when the drop in employment was matched by a rise in

unemployment.

And young people have been particularly affected, seeing disproportionate lay-offs

and delayed entry into the labour market. Research finds that this can have a variety

of long-lasting effects, including lower earnings ten to fifteen years later, and worse

future health conditions.

4

So, from the outset, this unusual recession has posed exceptionally high risks. That

is why an exceptional policy response has been required. And what has defined this

policy response, in Europe in particular, is the policy mix.

2

Beraja, M. and Wolf, C. (2020), “Demand Composition and the Strength of Recoveries”, mimeo.

3

Data from the ECB’s pilot Consumer Expectations Survey.

4

Von Wachter, T. (2020), “The Persistent Effects of Initial Labor Market Conditions for Young Adults and

their Sources”, Journal of Economic Perspectives, Vol. 34, No 4, pp. 168-194.

ECB Forum on Central Banking, November 2020

22

Learning the lessons of the last decade, there has been a renewed consensus that

the composition of policies matters for overcoming the crisis. More than ever before,

macroeconomic, supervisory and regulatory authorities have dovetailed and made

each other’s efforts more powerful.

3 Policy responses to the pandemic

What has this meant for monetary policy? There are two main ways in which we

have adapted the ECB’s policy to the pandemic: via the design of our tools and via

the transmission of our monetary policy.

First of all, we have responded to the unique features of the recession by designing

a set of tools specifically tailored to the nature of the shock, including recalibrating

our targeted longer-term refinancing operations (TLTROs), expanding eligible

collateral, and launching a new €1.35 trillion pandemic emergency purchase

programme (PEPP). The PEPP in particular has the dual function of stabilising

financial markets and contributing to easing the overall monetary policy stance,

thereby helping to offset the downward impact of the pandemic on the projected path

of inflation.

The stabilisation function of the PEPP is ensured by its flexibility, which is crucial

given the unpredictable course of the pandemic and its uneven impact across

economies. In this context, the PEPP’s flexibility allows us to react in a targeted way

and counter fragmentation risks. This was key in reversing the tightening of financing

conditions that we saw in the early days of the crisis.

In parallel, the stance function of the PEPP gives us the scope to counter the

pandemic-driven shock to the path of inflation – a path that has also been greatly

influenced by the specific characteristics of this recession. Not only has inflation

fallen into negative territory, but we have already seen services inflation, which is

normally the more stable part of the price index, drop to historic lows.

But the PEPP, together with the other measures we have taken this year, has

provided crucial support to the inflation path and prevented a much larger

disinflationary shock.

5

And its impact has been amplified by interactions with other

policies. For instance, the combined effect of the ECB’s monetary and supervisory

measures is estimated to have saved more than one million jobs.

6

At the same time, the nature of the pandemic also affects the transmission of

monetary policy. Normally, an easing of financing conditions boosts demand by

encouraging firms to borrow and invest, and households to bring forward future

5

Lagarde, C. (2020), “The monetary policy strategy review: some preliminary considerations”, speech at

the “ECB and Its Watchers XXI” conference, 30 September.

6

Altavilla, C., Barbiero, F., Boucinha, M. and Burlon, L. (2020), “The great lockdown: pandemic response

policies and bank lending conditions”, Working Paper Series, No. 2465, ECB, Frankfurt am Main,

September.

ECB Forum on Central Banking, November 2020

23

income and consume more. In turbulent times, monetary policy interventions also

eliminate excess risk pricing from the market.

But when interest rates are already low and private demand is constrained by design

– as is the case today – the transmission from financing conditions to private

spending might be attenuated. This is especially true when firms and households

face very high levels of uncertainty, leading to higher precautionary saving and

postponed investment.

7

In these circumstances, it is crucial that monetary policy

ensures favourable financing conditions for the whole economy: private and public

sectors alike. Indeed, these are the times when fiscal policy has the greatest impact,

for at least two reasons.

First, fiscal policy can respond in a more targeted way to the parts of the economy

affected by health restrictions. Research shows that, while monetary policy can

increase overall activity in this environment, it cannot support the specific sectors

that would be most welfare-enhancing. Fiscal policies, on the other hand, can

directly respond where help is most needed.

8

We have seen the efficacy of such targeting in the euro area this year. The ECB’s

Consumer Expectations Survey shows that households with lower income have seen

a greater reduction in the hours they work, but they have also received a higher

share of government support. As a result, while compensation of employees fell by

more than 7% in the second quarter, household disposable income fell by only 3%

9

,

because government transfers compensated for the loss of income.

Second, fiscal policy can break “paradox of thrift” dynamics in the private sector

when uncertainty is present. Public expenditure accounts for around 50% of total

spending in the euro area and can therefore act as a coordination device for the

other 50%. Our consumer survey demonstrates this: people who consider

government support to be more adequate display less precautionary behaviour. And

in this way, by brightening economic prospects for firms and households, fiscal policy

can help reinvigorate monetary transmission through the private sector.

4 The risk of an unsteady recovery

But regrettably the economic recovery from the pandemic emergency could well be

bumpy. We are seeing a strong resurgence of the virus and this has introduced a

new dynamic. While the latest news on a vaccine looks encouraging, we could still

face recurring cycles of accelerating viral spread and tightening restrictions until

widespread immunity is achieved.

7

Bloom, N., Bond, S. and Van Reenen, J. (2006), “Uncertainty and Investment Dynamics”, NBER

Working Paper Series, No 12383, National Bureau of Economic Research, July.

8

Woodford, M. (2020), “Effective Demand Failures and the Limits of Monetary Stabilization Policy”,

NBER Working Paper Series, No 27768, National Bureau of Economic Research, September.

9

Year-on-year changes.

ECB Forum on Central Banking, November 2020

24

So the recovery may not be linear, but rather unsteady, stop-start and contingent on

the pace of vaccine roll-out. In the interim, output in the services sector may struggle

to fully recover.

Indeed, services were already showing a declining trend before the latest round of

restrictions: the services PMI fell from 54.7 in July to 46.9 in October. And while

manufacturing has so far remained relatively resilient, there is a risk of the recovery

in manufacturing also slowing once order backlogs are run down and industrial

output becomes better aligned with demand.

In this situation, the key challenge for policymakers will be to bridge the gap until

vaccination is well advanced and the recovery can build its own momentum. The

strength of the rebound in the third quarter suggests that the initial policy response

was effective and the capacity of the economy to recover is still in place. But it will

require very careful policy management to ensure that this remains the case.

Above all, we must ensure that this exceptional downturn remains just that –

exceptional – and does not turn into a more conventional recession that feeds on

itself. Even if this second wave of the virus proves to be less intense than the first, it

poses no less danger to the economy.

In particular, if the public no longer sees the pandemic as a one-off event, we could

see more lasting changes in behaviour than during the first wave. Households could

become more fearful about the future and increase their precautionary saving. Firms

that have survived up to now by increasing borrowing could decide that remaining

open no longer makes business sense. This could trigger a “firm exit multiplier”,

where the closure of businesses faced with health restrictions cuts demand for

complementary businesses, in turn causing those firms to reduce their output.

10

If that were to happen, the recession could percolate through the economy to sectors

not directly affected by the pandemic – and potentially trigger a feedback loop

between the real economy and the financial sector. Banks might start tightening

credit standards in the belief that corporate creditworthiness is deteriorating, leading

to firms becoming less willing or able to borrow funds, credit growth slowing and

banks’ risk perceptions rising further. The ECB’s bank lending survey is already

signalling a possible tightening in the months to come. We are also seeing

indications that small and medium-sized firms are expecting their access to finance

to deteriorate.

A continued, powerful and targeted policy response is therefore vital to protect the

economy, at least until the health emergency passes. Concerns about

“zombification” or impeding creative destruction are misplaced, especially if a

vaccine is now in sight. Remember that lockdowns are a non-economic shock that

affects productive and unproductive firms indiscriminately. Policies that protect viable

10

Guerrieri, V., Lorenzoni, G., Straub, L. and Werning, I. (2020), “Macroeconomic Implications of COVID-

19: Can Negative Supply Shocks Cause Demand Shortages?”, NBER Working Paper Series, No

26918, National Bureau of Economic Research, April.

ECB Forum on Central Banking, November 2020

25

businesses until activity can return to normal will help our productive capacity, not

harm it.

The right policy mix is essential.

Fiscal policy has to remain at the centre of the stabilisation effort – the draft

budgetary plans suggest that fiscal support next year will be significant and broadly

similar to this year, and the Next Generation EU package should become operational

without delay. Supervisory authorities are working to ensure that banks can continue

to support the recovery by readying them for a potential deterioration in asset

quality.

11

And structural policies have to be stepped up so that policy support can

accompany the wide-ranging changes that the pandemic will bring, such as an

accelerating spread of digitalisation and a renewed focus on climate issues.

12

5 The outlook for monetary policy

So what is the role of monetary policy in this response?

It is clear that downside risks to the economy have increased. The impact of the

pandemic is now likely to continue to weigh on economic activity well into 2021.

Moreover, demand weakness and economic slack are weighing on inflation, which is

expected to remain in negative territory for longer than previously thought. This is

partially due to temporary factors, but the fall in measures of underlying inflation also

appears to be connected to the weakening of activity. And developments in the

exchange rate may have a negative impact on the path of inflation.

Continued policy support is therefore necessary to achieve our inflation aim. But we

should also consider how best to provide that support.

The unusual nature of the recession and the unsteadiness of the recovery make

assessing the inflation path harder than in normal times. Shifts in consumption

baskets caused by supply-side restrictions are creating significant noise in the

inflation data.

13

And the stop-start nature of the recovery means the short-term path

of inflation is surrounded by considerable uncertainty.

In these conditions, it is vital that monetary policy underpins inflation dynamics by

supporting demand and preventing second-round effects, where the negative

pandemic shock to inflation feeds into wage and price-setting and becomes

persistent. To that end, the best contribution monetary policy can make is to ensure

favourable financing conditions for the whole economy. Two considerations are

important here.

11

Enria, A. (2020), “Supervisory challenges of the pandemic and beyond”, speech at the Handelsblatt

European Banking Regulation Conference, 3 November.

12

Lagarde, C. (2020), “Remarks at the G30 International Banking Seminar”, contribution during the

session “Rebuilding and Sustaining Growth”, 18 October.

13

Kouvavas, O. et al. (2020), “Consumption patterns and inflation measurement issues during the

COVID-19 pandemic”, Economic Bulletin, Issue 7, ECB, November.

ECB Forum on Central Banking, November 2020

26

First, while fiscal policy is active in supporting the economy, monetary policy has to

minimise any “crowding-out” effects that might create negative spillovers for

households and firms. Otherwise, increasing fiscal interventions could put upward

pressure on market interest rates and crowd out private investors, with a detrimental

effect on private demand.

Second, monetary policy has to continue supporting the banking sector to secure

policy transmission and prevent adverse feedback loops from emerging. Firms are

still dependent on new flows of credit. And those that have borrowed heavily so far

need certainty that refinancing will remain available on attractive terms in order to

avoid excessive deleveraging.

In other words, when thinking about favourable financing conditions, what matters is

not only the level of financing conditions but the duration of policy support, too. All

sectors of the economy need to have confidence that financing conditions will remain

exceptionally favourable for as long as needed – especially as the economic impact

of the pandemic will now extend well into next year.

Currently, all conditions are in place for both the public and private sectors to take

the necessary measures. The GDP-weighted sovereign yield curve is in negative

territory up to the ten-year maturity. Nearly all euro area countries have negative

yields up to the five-year maturity. Bank lending rates are close to their historic lows:

around 1.5% for corporates and 1.4% for mortgages. And our forward guidance on

our asset purchase programmes and interest rates provides clarity on the future path

of interest rates.

But it is important to ensure that financing conditions remain favourable. This is why

the Governing Council announced last month that we will recalibrate our instruments,

as appropriate, to respond to the unfolding situation. The Council is unanimous in its

commitment to ensure that financing conditions remain favourable to support

economic activity and counteract the negative impact of the pandemic on the

projected inflation path.

In the weeks to come we will have more information on which to base our decision

about this recalibration, including more evidence on the success of the new

lockdown measures in containing the virus, a new set of macroeconomic projections

and more clarity on fiscal plans and the prospects for vaccine roll-outs.

While all options are on the table, the PEPP and TLTROs have proven their

effectiveness in the current environment and can be dynamically adjusted to react to

how the pandemic evolves. They are therefore likely to remain the main tools for

adjusting our monetary policy.

Looking beyond our next policy meeting, our ongoing strategy review gives us an

opportunity to reflect on the best combination of tools to deliver financing conditions

at the appropriate level, how those tools should be implemented, and what features

our toolkit needs to have to deliver on such a strategy.

ECB Forum on Central Banking, November 2020

27

6 Conclusion

Let me conclude.

The pandemic has produced an unusual recession and will likely generate an

unsteady recovery. All policy areas in Europe have responded promptly and

decisively. The European policy mix has proven that when different authorities work

together – within their respective mandates – countries can successfully absorb the

pandemic shock.

The second wave of COVID-19 presents new challenges and risks, but the blueprint

for managing it is the same. The ECB was there for the first wave and we will be

there for the second wave. We are, and we continue to be, totally committed to

supporting the people of Europe.

In pursuit of our mandate, we will continue to deliver the financing conditions

necessary to protect the economy from the impact of the pandemic. This is the

precondition for stabilising aggregate demand and securing the return of inflation to

our aim.

ECB Forum on Central Banking, November 2020

28

De-globalisation? Global value chains in

the post-COVID-19 age

By Pol Antràs

1

Abstract

Although the growth of international trade flows relative to that of GDP has slowed

down since the Great Recession, this paper finds little systematic evidence indicating

that the world economy has already entered an era of de-globalisation. Instead, the

observed slowdown in globalisation is a natural sequel to the unsustainable increase

in globalisation experienced in the late 1980s, 1990s and early 2000s. I offer a

description of the mechanisms leading to that earlier expansionary phase, together

with a discussion of why these forces might have run out of steam, and of the extent

to which they may be reversible. I conclude that the main challenge for the future of

globalisation is institutional and political in nature rather than technological. Zooming

in on the COVID-19 global pandemic, I similarly conclude that the current health

crisis may further darken the future of globalisation if it aggravates policy tensions

across countries.

1 Introduction

At the time of writing, the world is witnessing extraordinary events. The COVID-19

global pandemic has brutally awakened the world from a Panglossian tranquillity

caused by decades of relatively sporadic and largely isolated epidemic risks. The

magnitude and nature of the COVID-19 shock has quickly spilled over to the global

economy, triggering a dramatic decline in economic activity, due both to social

distancing practices but also due to government-mandated lockdowns and other

mobility restrictions.

In describing the unfolding and the consequences of the current COVID-19 health

crisis, journalists and commentators have been using the word “unprecedented” with

a frequency that is unprecedented. One example of such hyperbolic commentary is

the notion that the world economy has now entered a phase of de-globalisation in

which economic agents are increasingly severing their international economic links

1

Harvard University. This paper was written for the ECB Forum on Central Banking, “Central Banking in

a Shifting World,” originally scheduled to take place in Sintra, Portugal, in June 2020. I am grateful to

Jingyi Tao for outstanding research assistance, to Max Alekseev, Davin Chor, Evgenii Fadeev, Elhanan

Helpman, and Steve Redding for detailed comments, to Gita Gopinath and Şebnem Kalemli-Özcan for

helpful discussions, and to Diego Cerdeiro, Michael Clemens, Lionel Fontagné, Michele Mancini,

Sébastien Miroudot, and Josep Pijoan-Mas for sharing data with me. The author received an

honorarium for carrying out and presenting the research in this paper.

ECB Forum on Central Banking, November 2020

29

and are reshoring economic activity toward their domestic economies. Is the world

economy really getting de-globalised?

Ironically, such an unravelling of globalisation would not be unprecedented. The last

significant episode of de-globalisation occurred in the 20th century during the so-

called Interwar Period, a period which coincidentally witnessed at its onset one of the

most devastating global pandemics on record, the 1918 Influenza Pandemic.

2

Of

course, there are a myriad of forces that contributed to the de-globalisation of the

Interwar Period, none more important than (i) the belligerent and dysfunctional

political world order that emanated from World War I, and (ii) a worldwide economic

downturn – the Great Depression – that severely impacted many of the world’s

largest economies and led these countries’ governments to institute beggar-thy-

neighbour policies.

Luckily, the world has not witnessed a truly global military conflict since 1945. Yet the

Great Recession of the late 2000s brought to an abrupt halt the process of

globalisation that had begun in the post-war period and that had accelerated

remarkably in the mid-1980s. And, much as happened during the Interwar Period,

the recent Great Recession has rekindled nationalistic sentiments in many advanced

countries, fuelling a political rhetoric that blames foreigners for the economic woes

faced by the domestic residents of these advanced countries. Although the extent to

which this rhetoric has materialized into actual policies has been somewhat limited,

the recent trade disputes between the U.S. and China and the withdrawal of the

United Kingdom from the European Union have shaken the firm ground over which

the process of globalisation appeared to be cemented. To cap it all, since early 2020

the world economy has submerged itself into a global health crisis that, due to its

severity and asynchronous nature, has dramatically impacted the functioning of

global value chains.

In sum, in an era like the present one with significant health, economic and policy

uncertainty, it is natural that some commentators have spotted the beginnings of a

new era of de-globalisation.

3

The goal of this paper is to try to elucidate whether the

world economy might have indeed already entered such a phase of de-globalisation

and, more speculatively, to offer some thoughts on the future of global value chains

in the post-COVID-19 age.

The paper sets off, in section 2, by studying the process of globalisation in recent

decades. Unlike the view pushed by some commentators, the paper argues that

there is no conclusive evidence indicating that the world economy is significantly less

global today than it was at the onset of the Great Recession. It is certainly the case

that that pace of globalisation has slowed down relative to recent decades – a

process that The Economist has referred to as Slowbalisation

4

– but the anecdotal

2